The global carbon credit market is undergoing a structural shift as aviation compliance demand increases and high-quality supply becomes more constrained.

According to Sylvera’s Carbon Data Snapshot for Q1 2026, total credit retirements fell by 8% year-on-year, with total market value declining from $309.47m to $290m. Despite this drop in volume, pricing trends indicate a move toward higher-quality credits.

The average price per credit rose slightly to $5.69, up from $5.60 a year earlier. Investment-grade credits are commanding significantly higher premiums, with BBB+ credits averaging $20.10, compared to $7.80 for lower-rated B credits. Combined AA, A and BBB credits now account for 62% of total rated market value.

High-rated REDD+ credits have continued their upward trajectory, rising for a third consecutive quarter to $9.60, while lower-rated equivalents remain stable at $3.70.

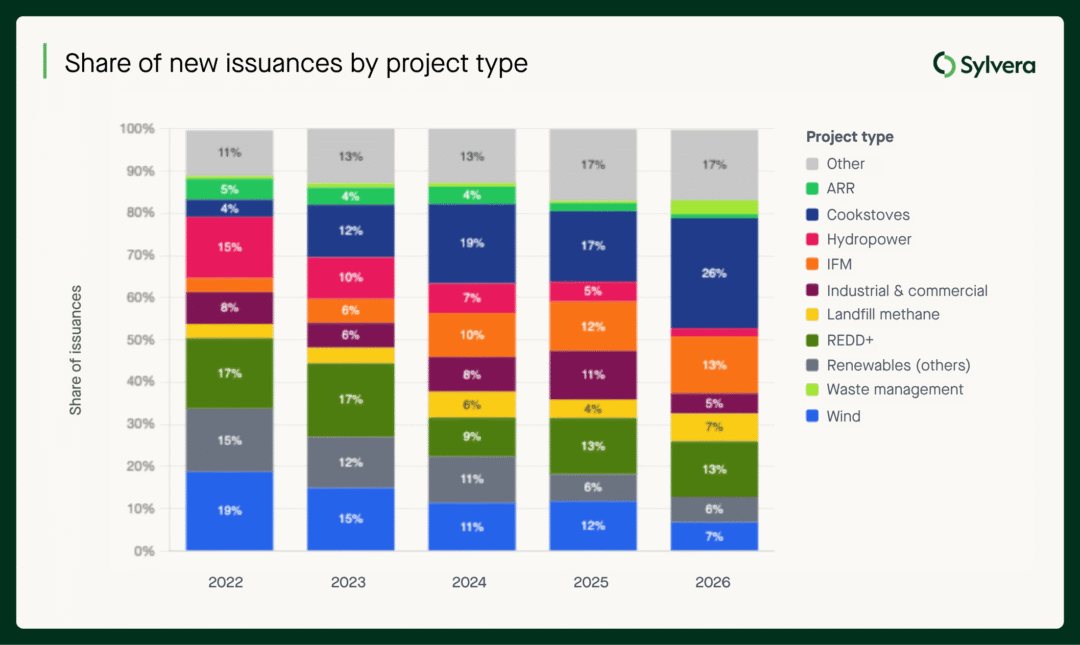

For the first time, credits eligible under CORSIA — the aviation sector’s global offsetting scheme — represent nearly half of new issuances. However, while compliance-eligible supply is increasing, actual usable supply remains constrained due to regulatory bottlenecks, particularly under Article 6 mechanisms.

At the same time, Core Carbon Principles accreditation has expanded significantly, rising from less than 3% of issuances in 2023 to 18% in early 2026. The price premium for CCP-aligned credits has more than doubled to $3.83.

New project categories are also reshaping supply. Clean water initiatives have grown rapidly, reaching 8.2 million credits annually, while marine and mangrove projects now account for 5.3 million credits. Nitrous oxide destruction projects have expanded sharply, and regenerative agriculture has emerged as one of the fastest-growing segments.

Sylvera chief executive Allister Furey said the market is increasingly defined by quality, compliance readiness and methodological rigour, with a growing divide between investment-grade credits and legacy supply.

Looking ahead, supply constraints are expected to intensify. While demand continues to rise — particularly from compliance markets — the availability of deliverable, high-quality credits remains limited.