Global air cargo capacity continues to recover and has moved closer again to the levels recorded a year earlier, according to the latest figures released by consultant Aevean.

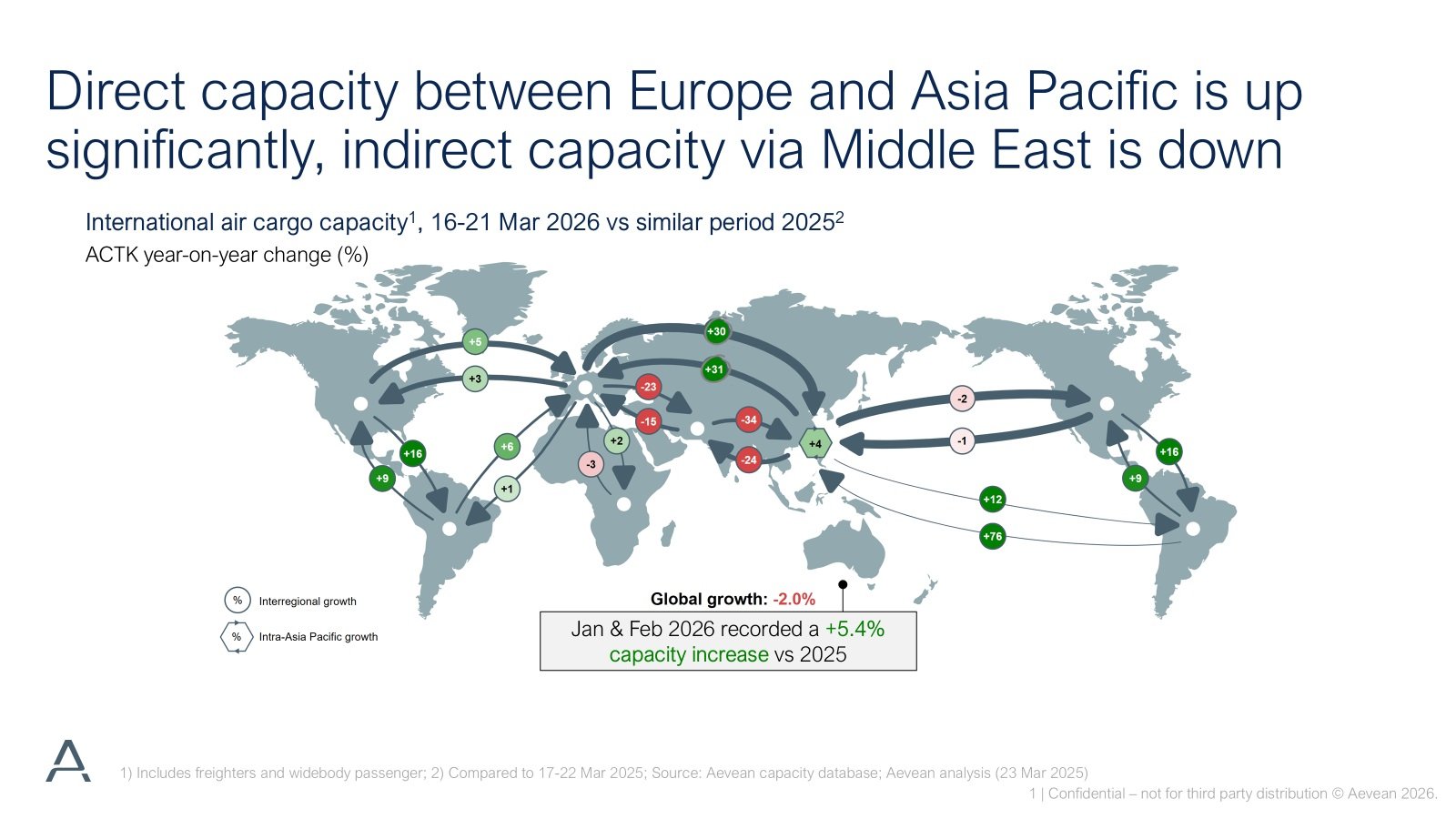

The company said international air cargo capacity worldwide was just 2% below the equivalent period last year during the most recent week measured.

At the height of the crisis, when carriers were dealing with widespread airspace closures across the Middle East, cargo capacity had fallen by around 20% compared with the previous year.

Since then, affected airlines in the Middle East have gradually resumed operations. Most recently, Qatar Airways Cargo, the world’s largest air cargo carrier, announced an increase in services. From 21 March, the airline reinstated a freighter schedule covering destinations in Vietnam, China, Thailand, South Korea, Nigeria, Kenya, Germany, the Netherlands, Belgium, the US, Brazil, Ecuador and Panama.

Aevean cautioned, however, that the headline recovery should be viewed with some nuance. While global cargo capacity is now only down 2% year on year, the January and February data showed that before the outbreak of fighting in the Middle East, capacity had actually been running 5.4% higher than a year earlier, in response to demand growth of around 6% to 7%.

That means capacity may be closing the gap with last year’s level but could still be lagging behind the demand increase seen so far in 2026, which would continue to place pressure on load factors.

Regional disparities also remain pronounced. Aevean said capacity into and out of the Middle East is still well below last year’s levels. Capacity from Asia Pacific into the region is down 24% year on year, while capacity from the Middle East to Europe has declined by 15%.

At the same time, carriers have been shifting capacity onto Asia Pacific-Europe services to offset the shortfall of traffic that would normally move into Europe via the Middle East. As a result, Aevean recorded a 31% increase in capacity from Asia Pacific to Europe.