Global air cargo spot rates are rising sharply as the conflict in the Middle East continues to disrupt capacity, alter routing patterns and drive up fuel costs across the market.

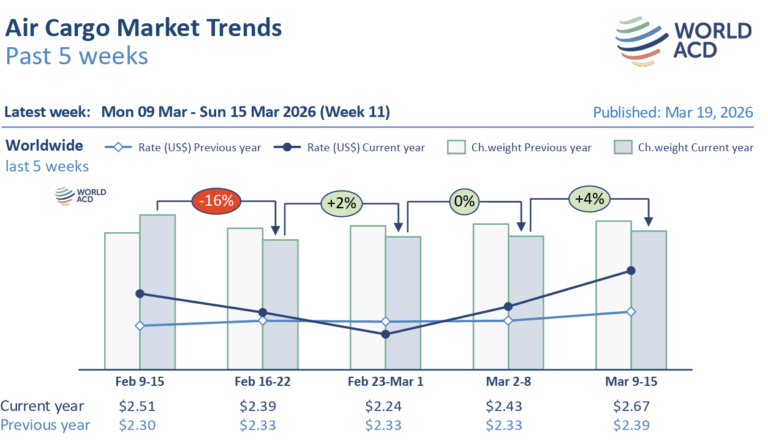

According to the latest data from WorldACD Market Data, average full-market air cargo rates rose by 10% week on week in week 11, covering 9 to 15 March, reaching $2.67 per kilo including surcharges. That followed an 8% increase the previous week, highlighting the speed at which carriers, freight forwarders and cargo owners are reacting to disrupted conditions, constrained capacity, backlog pressure, alternative routings and higher jet fuel prices.

The broader market has shown some recovery since the outbreak of war, but the operating environment across the Middle East remains highly unstable and subject to sudden change for carriers, airports and logistics stakeholders.

WorldACD’s figures, based on more than 500,000 weekly transactions, also show global volumes rising 4% week on week. That increase was driven by further post-Lunar New Year recovery in Asia Pacific, where volumes climbed 5%, and by a partial rebound from Middle East and South Asia origins, where tonnages rose 30%. Even so, global cargo volumes remained 7% below the same period last year, underlining the continued weakness in the overall market.

Spot rates increased even more sharply than overall rates. Worldwide spot levels rose 12% week on week to $3.19 per kilo, putting them 22% above the equivalent week last year.

The strongest rate spikes came from Middle East and South Asia origins. Spot rates from the region surged another 22% week on week to $4.37 per kilo, leaving them 58% above the level recorded a year earlier.

Although some capacity and traffic recovered last week as certain airports and airspace partially reopened and carriers used alternative routings, services to and from the region remain heavily constrained — particularly within Gulf countries — and continue to face delays, backlogs and abrupt disruption.

The 30% rebound in tonnages from Middle East and South Asia origins followed a 33% fall the previous week, when regional capacity collapsed by 50%. With some limited capacity returning last week, up 35% week on week, cargo volumes from Gulf area countries surged 74% after having fallen 65% the week before. Even so, volumes remain roughly 50% below their pre-war levels, based on the week of 16 to 22 February.

Spot rates from Gulf countries rose another 22% week on week to $3.77 per kilo, placing them about 56% above their pre-war level.

South Asian origins also saw a partial rebound, with tonnages increasing 24% week on week. Still, those volumes remain 20% below pre-war levels. Spot rates from South Asia rose 24% to $3.54 per kilo, meaning they have climbed by more than 60% in just two weeks.

On the Middle East and South Asia to Europe corridor, volumes rose 27% week on week, but they remain 20% below pre-war levels and 9% below last year’s level for the same period. Dubai showed a particularly strong rebound, with tonnages up 67% after falling 39% the previous week, although they are still 30% below the pre-war benchmark.

Rates on the corridor rose even faster. Spot rates from Middle East and South Asia origins to Europe jumped 21% week on week, on top of the previous week’s 60% rise. That leaves them 70% above last year’s level and nearly double their pre-war level. From Dubai specifically, rates rose a further 9% after soaring 90% the week before, reaching $3.93 per kilo — more than twice both last year’s level and the pre-war benchmark.

A similar dynamic is playing out on services to the United States. Volumes from Middle East and South Asia origins to the US climbed 22% week on week, though they remain 20% below pre-war levels and 2% below last year’s equivalent period. Spot rates on that corridor increased another 25% on top of a 30% rise the week before, leaving them 50% above last year and more than 65% above pre-war levels. Rates from Dubai to the US surged by another 56% to $8.46 per kilo after nearly 50% growth the week before, putting them around 2.5 times higher than last year and well above pre-war levels.

The situation remains extremely volatile. Since the end of last week, new restrictions have further affected capacity to and from the United Arab Emirates, where only UAE-based carriers are currently allowed to operate flights following a drone strike on a fuel terminal that severely constrained jet fuel availability.

At the same time, Qatar Airways Cargo announced on 19 March that it planned to resume selected freighter operations to and from Doha, where services had been suspended for the previous three weeks, while continuing some limited freighter activity outside the Qatari capital.

Jet fuel has become a central pressure point. The effective blockade of the Strait of Hormuz has pushed jet fuel prices up another 11% week on week, taking them to nearly double — 94% above — their pre-war level. In response, carriers have introduced additional fuel surcharges, and some have also applied war-risk surcharges, both of which are feeding directly into the rise in overall air cargo rates.

Outside the Middle East, Asia Pacific continued its post-Lunar New Year recovery. Volumes from the region rose another 5% week on week, leaving them around 30% above the level seen at the start of the holiday period in week 8, although still 12% below pre-holiday levels. Spot rates from Asia Pacific rose 9% to $3.94 per kilo, placing them 12% above last year.

Asia Pacific to US volumes edged up 3% after a 17% surge the previous week, supported by continuing post-holiday recovery and strong increases from China and Hong Kong. Volumes on that corridor are now only 4% below last year’s level. Spot rates also climbed strongly, rising 8% week on week, with all major origin markets except Japan recording gains.

On Asia Pacific to Europe, volumes increased another 5% following the previous week’s 17% rise. Despite that recovery, they remain 12% below the same period last year, although comparisons are affected by the earlier Lunar New Year timing in 2025. Spot rates to Europe have been hit even more strongly by the Middle East crisis than those to the US, rising 13% week on week after a 12% increase the week before. Every major Asia Pacific origin market saw rates move higher, although increases from Singapore and South Korea were more modest than elsewhere.