The global airfreight market is once again being pushed into a high-pressure environment as the conflict in the Middle East adds fresh uncertainty to an already fragile 2026 outlook. According to Xeneta, the industry is showing short-term resilience, helped by stronger collaboration between shippers, airlines and forwarders, but the longer the disruption continues, the greater the risk to demand and the broader economy.

Air cargo has often acted as the supply chain’s relief valve during crises, stepping in when ocean freight came under strain during Covid or the Red Sea disruption. This time, however, the pressure is falling more directly on airlines and the air cargo sector itself. Xeneta chief airfreight officer Niall van de Wouw said the industry is less focused on whether demand slipped by 2% or 4% in March than on the much larger question of whether the market is moving toward a deeper global economic shock.

Van de Wouw said rates are rising and pricing is already being reshaped by the conflict, but for shippers, transport cost is only one factor. Protecting customer relationships and preserving market share remain equally important. He warned that higher fuel prices may not hit demand immediately, but could do so if the crisis becomes a long-term drag on the global economy. For now, the sector is continuing to move cargo, albeit at a higher cost, with capacity shifting toward safer gateways such as Muscat and Jeddah.

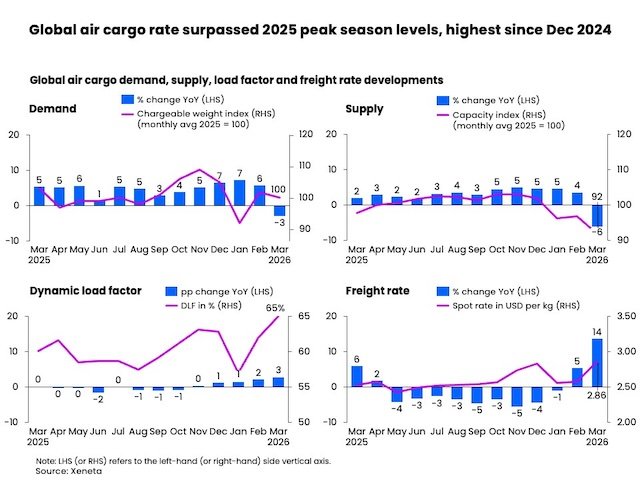

The market backdrop remains deeply unstable. Dubai and Doha, long central to global air cargo connectivity through carriers such as Emirates, Etihad and Qatar Airways, have become more exposed as the region’s geographic advantage turns into a strategic vulnerability. Five weeks into the conflict, regional air cargo capacity remained about 30% below pre-conflict levels. That squeeze has fed directly into pricing, with global spot rates in March climbing to $2.86 per kg, above 2025 peak-season levels and the highest since December 2024.

The timing has also complicated annual contract negotiations. The conflict intensified during tender season, accelerating a shift already visible in the first quarter, as shippers moved more decisively toward shorter three-month agreements rather than annual contracts. Xeneta had already advised customers to delay tenders given the speed at which market conditions were changing. In March, 52% of global air cargo volumes moved under spot pricing, just one point below the level seen at the start of the pandemic.

The sharpest increases have been seen on outbound lanes from South Asia and Southeast Asia to the Middle East, where spot rates jumped by 50% to 100% in the week ending 29 March compared with four weeks earlier. Xeneta linked the surge to severe capacity shortages, airlines’ reliance on Middle Eastern networks, much higher jet fuel costs and war-risk surcharges. The disruption is also spilling well beyond the region, affecting Asia-Europe, Europe-Africa and transpacific corridors, although some Northeast Asia-Europe routes have held up better thanks to greater use of direct services.

Longer-term contract rates tell a more cautious story. On some Asia-North America lanes, rates valid for more than a month rose only modestly, as US tariffs and the end of de minimis exemptions continued to weigh on demand. Other routes have moved differently again, with Europe-North America spot rates falling as summer passenger schedules restored bellyhold capacity, while Europe-Latin America rates edged higher.

Xeneta believes the market’s current stress is still primarily a supply-side issue, but warns that the longer the crisis lasts, the more likely it is to turn into a full demand problem. Global air cargo demand fell 3% year on year in March, while capacity was down 6% compared with the same month in 2025. Dynamic load factor rose to 65%, showing that available space is being used more intensely even as the market waits to see whether this conflict becomes a short shock or a deeper structural break.