The air cargo sector is holding up for now amid the Middle East conflict, but the longer-term outlook is becoming more fragile as higher fuel costs and operational disruption start to weigh on the market, according to Xeneta.

The freight rate benchmarking and market intelligence platform said airlines and forwarders are still seeing resilient demand as shippers continue to prioritise customer service and market share, even as transport costs rise. For the moment, that has helped create a degree of short-term stability, with market participants waiting to see how the geopolitical situation evolves and what the broader economic consequences may be.

Niall van de Wouw, Xeneta’s chief airfreight officer, said there is widespread concern about what comes next, but also a more constructive and transparent relationship between customers and suppliers. He noted that many stakeholders understand the disruption is outside their control and are working together to keep cargo moving.

Even so, Xeneta warned that airfreight is feeling the impact of the conflict more directly than ocean shipping. Rates are already rising, and van de Wouw said there are clear signs that the conflict is reshaping air cargo pricing worldwide. He added that any demand destruction may not be immediate, but if the conflict drags on, the effect of more expensive fuel and wider economic pressure could significantly weaken airfreight demand.

There may also be some temporary upside for air cargo as ocean carriers declare “end of voyage” at ports short of their intended destination, forcing shippers and forwarders to rebuild supply chains using alternative modes. But Xeneta believes that any such gains are likely to be short-lived.

March figures underline the pressure building in the market. Global air cargo demand fell 3% year on year, while capacity was down 6% compared with March 2025. Xeneta’s dynamic load factor, which measures capacity utilisation by both weight and volume, climbed to 65%.

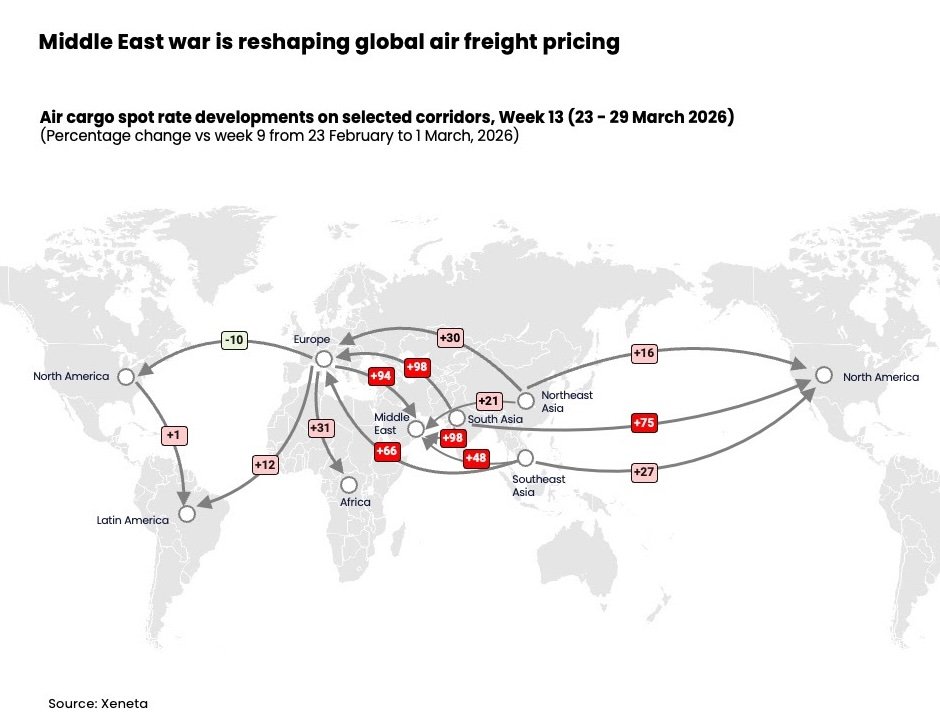

In the Middle East region, air cargo capacity remains around 30% below pre-conflict levels. At the same time, global spot rates in March reached $2.86 per kg, surpassing last year’s peak-season highs and marking their strongest level since December 2024.

The uncertainty is also changing buying behaviour. Xeneta said shippers have leaned toward shorter three-month agreements during the first quarter rather than annual contracts, compressing rate validity across the market. Van de Wouw said the company has advised customers to delay tenders where possible, arguing that long-term commitments offer little value when market conditions can shift so quickly.

Negotiations between airlines and forwarders are also beginning to resemble the dynamics seen during the Covid period. In March, 52% of global cargo volumes moved under spot rates, up three percentage points month on month and only one point below the level recorded at the start of the pandemic.

Some of the sharpest rate increases have been seen on outbound lanes from South Asia and Southeast Asia to the Middle East, where spot prices jumped by 50% to 100% in the week ending 29 March compared with four weeks earlier. Xeneta attributed the surge to a combination of severe capacity shortages, the heavy role of Middle Eastern carriers, nearly doubled jet fuel costs and new war-risk surcharges.

The disruption is now affecting much broader trade flows. The Middle East accounts for roughly half of the available capacity on Asia-Europe corridors, as well as key South Asia-Americas connections, meaning changes in the region are now reshaping pricing and routing across entire lane systems.

Rates from Southeast Asia and South Asia to Europe have moved in a similar direction because of the dominance of Middle Eastern carriers on those trades. Northeast Asia-Europe has held up better, helped by the deployment of additional direct services. Europe-Africa rates, meanwhile, have risen 31%, reflecting the Middle East’s role as the main transit point between the two regions.

Five weeks into the crisis, the impact has spread well beyond Asia-EMEA lanes. Higher fuel costs have pushed rates from Northeast Asia and Southeast Asia to North America up by mid- to high-double-digit percentages. South Asia-North America rates have climbed even more sharply, rising by around 75%, again due to the strong presence of Middle Eastern operators on that corridor.

Longer-validity rates, however, tell a more nuanced story. On Northeast Asia and Southeast Asia-North America trades, rates valid for more than a month rose only by low single digits over the same four-week period. Xeneta said that softer demand linked to US tariffs and the rollback of de minimis exemptions is continuing to weigh on those markets.

Not every trade lane is moving higher. Europe-North America spot rates fell around 10% in the week ending 29 March compared with four weeks earlier, as the start of summer passenger schedules restored additional bellyhold cargo capacity. North America-Latin America rates were broadly stable, while Europe-Latin America rates rose by around 12% after capacity was withdrawn from that market.

Van de Wouw said the duration of the conflict will ultimately determine whether this remains a supply-side shock or turns into a more damaging demand problem. He argued that while tariffs created uncertainty, the consequences of this crisis are potentially more severe because of the impact on fuel prices, energy markets and inflation.

For now, he said, air cargo is facing a capacity and supply challenge that should eventually ease. But if recovery takes too long, it could turn into a much broader demand issue, with the long-term outcome for airfreight depending on both the duration of the conflict and how it ends.