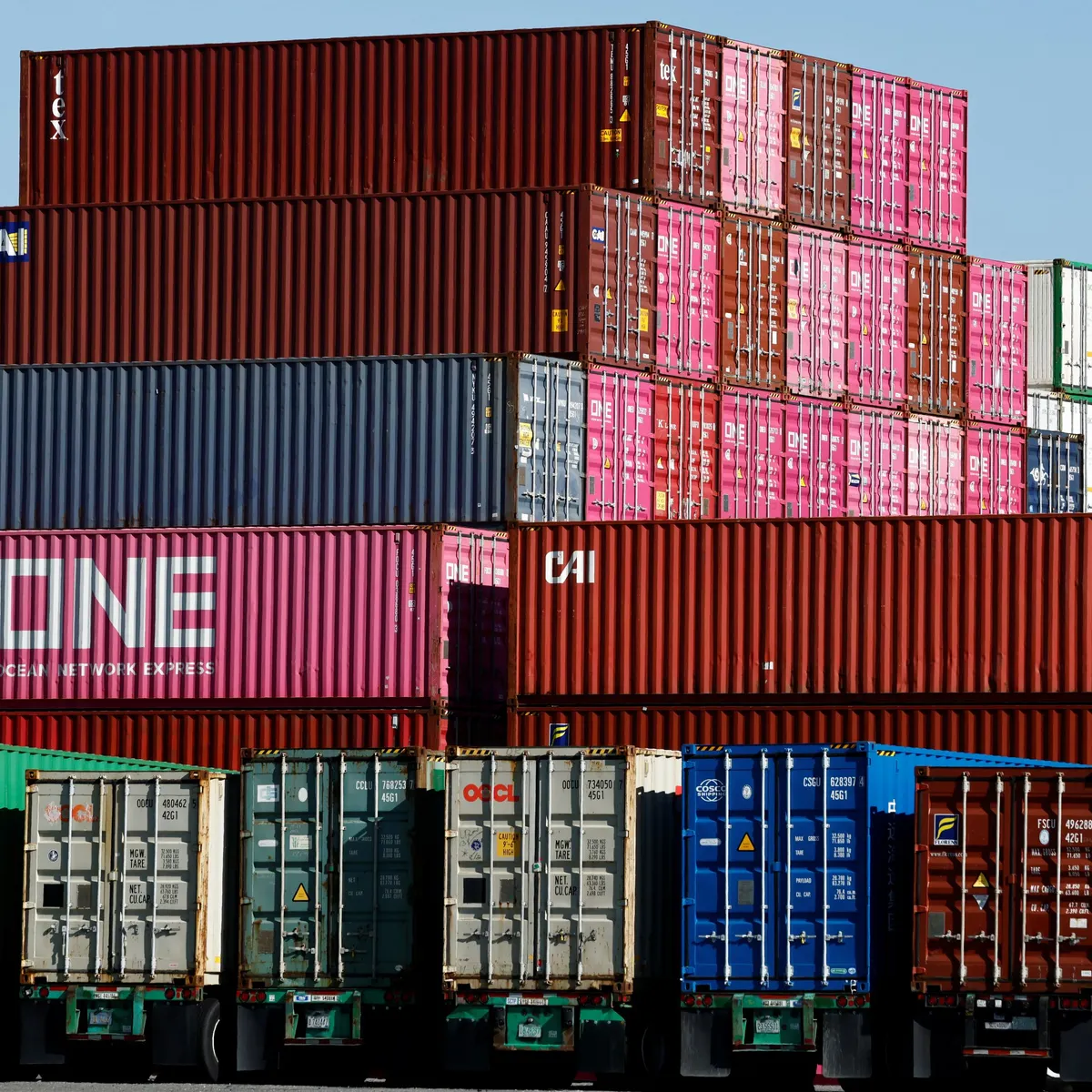

One year after the introduction of the so-called “Liberation Day” tariffs, global packaging supply chains remain under significant pressure, with manufacturers and consumer brands still struggling to adapt to an increasingly unstable environment.

Initially imposing a baseline 10% tariff on nearly all imports before being rolled back, the policy has left a lasting impact on sourcing strategies. More recently, the U.S. administration adjusted duties again—reducing tariffs on steel, aluminum and copper derivatives, while maintaining a 50% rate on products largely composed of those materials, such as food and beverage cans.

At the same time, the 2026 Iran war is compounding the disruption, driving up costs and intensifying volatility across the packaging sector.

“These black swan events keep coming at us,” said Jason Wong, founder and CEO of packaging manufacturer Paking Duck. “We just don’t have time to prepare.”

Despite mounting pressure, most consumer goods companies have only made limited adjustments. Some have explored domestic sourcing options where possible or increased inventory levels to hedge against further disruptions. However, in most cases, supply chains remain largely unchanged, with brands either absorbing rising costs or passing them on to consumers.

According to Wong, many companies feel they have already exhausted available options and are now in a wait-and-see position.

Limited flexibility despite rising costs

For smaller players, the impact is even more pronounced.

Shubhangini Prakash, founder of skincare brand Feather & Bone, said her company had to adapt its sourcing strategy following the tariff shifts of 2025. Working primarily through distributors, she introduced alternative suppliers when component costs increased.

The effect on pricing has been dramatic. Packaging for one of her products—sold in a twist tube similar to a deodorant—rose from approximately $0.80 to $3 per unit.

“$3 for a piece of packaging that’s plastic is really insane, but that’s where we are right now,” she said.

To offset these increases, Prakash has explored alternative distribution models, including partnerships with refill stores, where customers bring their own containers. However, she acknowledged that such solutions remain marginal and cannot replace traditional single-use packaging at scale.

Following the initial tariff announcements, Paking Duck responded by stockpiling packaging materials and renegotiating raw material costs with suppliers, including ink providers. Even so, uncertainty around trade policy has already affected customer behaviour, with some clients shifting to domestic suppliers to mitigate risk.

Yet, according to Wong, fully relocating production to the United States is not a viable solution.

“Manufacturing practices in China have been perfected in the last few decades. You can’t just bring that to America and call it a day,” he said, noting that domestic alternatives often come at significantly higher costs.

Structural limits to reshoring

Industry experts confirm that the idea of fully reshoring packaging supply chains remains largely theoretical.

Tom Hammann, owner of consulting firm WTH Solutions, said that while tariffs often trigger calls for domestic production, the reality is far more complex. Certain materials are simply not available in the U.S., and any packaging redesign requires extensive testing before deployment.

Prakash echoed this constraint, noting that during her search for packaging suppliers, several U.S. manufacturers confirmed that certain products—such as metal tins—are only produced in China.

As a result, her company has chosen to maintain its existing packaging design while absorbing higher costs rather than increasing retail prices.

“You’re really at a ceiling of how much you can forward this price to the customer before you start to alienate them,” she said.

While tariffs have accelerated cost-cutting initiatives, supply chain optimisation in packaging is not new. According to Hammann, companies have already spent years improving efficiency—through measures such as reducing material usage or redesigning packaging formats.

More recently, brands have also invested in better supply chain visibility and supplier mapping, allowing them to respond more quickly when disruptions occur.

War-driven cost escalation adds further pressure

Beyond tariffs, the Iran conflict is introducing a new layer of complexity.

Rising oil prices are directly impacting petroleum-based plastics, while alternative materials often fail to meet functional requirements. As Wong pointed out, replacing plastic with paper or metal is not feasible for many applications, such as liquid packaging.

Moreover, switching materials is not a short-term solution. Any change requires validation across manufacturing, logistics and distribution processes.

“You have to test it in the manufacturing plant. You have to make sure it gets through the distribution chain,” Hammann explained.

The broader logistics environment is also affected. Shipping costs have surged, with Transpacific rates rising nearly 30% between late February and early April, further increasing pressure on packaging costs.

While plastic is the most directly impacted, Wong expects a ripple effect across other materials as energy and transport costs feed through the system.

In response, some companies are simplifying packaging designs or increasing inventory levels ahead of anticipated price hikes.

Still, the overall outlook remains uncertain.

According to Hammann, companies are effectively adopting a dual strategy: “hope for the best, plan for the worst.”

Major industry players are already bracing for continued volatility. Lamb Weston expects ongoing fluctuations in packaging costs, while Lindt & Sprüngli anticipates a medium-term increase driven by fuel and logistics expenses.