Container shipping markets are feeling the global impact of the closure of the Strait of Hormuz, with spot rates climbing sharply across major east-west trade lanes, including routes serving the United States.

According to Xeneta chief analyst Peter Sand, the conflict is no longer a regional shipping issue but a broader supply chain event with worldwide repercussions. Five weeks into the disruption, he said, spot rates have risen on every major east-west lane, including trades far removed geographically from the Gulf.

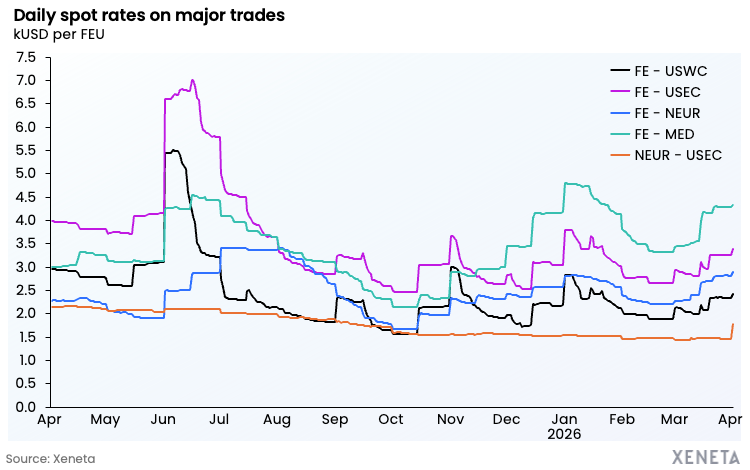

Far East to US West Coast rates have climbed 29% since the end of February, despite the route crossing the Pacific far from the conflict zone. Xeneta said that reflects growing shipper concern over operational disruption and cost escalation across the global network.

On trades more directly exposed to Middle East disruption, rates have risen even further. Spot prices from the Far East to North Europe were up 31%, while Far East to Mediterranean services recorded a 30% increase over the same period.

Xeneta said port congestion in the Middle East has also spread to major Asian transshipment hubs such as Singapore, Port Klang and Tanjung Pelepas, all of which play a key role in feeding cargo into long-haul services, including routes bound for the US.

Sand said memories of the Red Sea crisis in 2024 remain fresh for shippers, even on trades that do not directly transit conflict zones. He said carriers have made it clear that the cost of uncertainty will be passed on to shippers, and that many cargo owners are now paying more to lock in capacity rather than risk even higher prices during peak season.

As of 1 April, Xeneta recorded average market spot rates of $2,430 per 40ft container from Asia to the US West Coast, $3,382 to the US East Coast, and $1,775 from North Europe to the US East Coast.

Despite wider concern, fuel availability has not yet become a major constraint for vessels. Xeneta said bunker fuel remains available in Singapore, the world’s largest bunkering hub, although prices are roughly double pre-crisis levels. Those prices have eased slightly after an initial spike of around 200%. In Rotterdam, fuel prices continue to trend upward, while ship-to-ship transfers in the Far East are adding further cost and complexity.

Sand said that if the crisis continues without resolution, carriers are likely to prepare additional contingency measures. The coming weeks, he said, will show whether slow steaming and rerouting can absorb the disruption, or whether blank sailings become the next tool used to manage capacity and pricing.

Separately, Maersk has again asked the US Federal Maritime Commission to waive the normal 30-day waiting period for emergency fuel surcharge implementation. A previous request from Maersk and other carriers was rejected in late March, with a new ruling expected imminently.