The International Energy Agency’s (IEA) latest monthly report, released Wednesday, presents a mixed outlook for oil markets following the U.S.–Iran peace agreement, offering arguments that can be interpreted as both bearish and bullish depending on how supply risks evolve in the coming months.

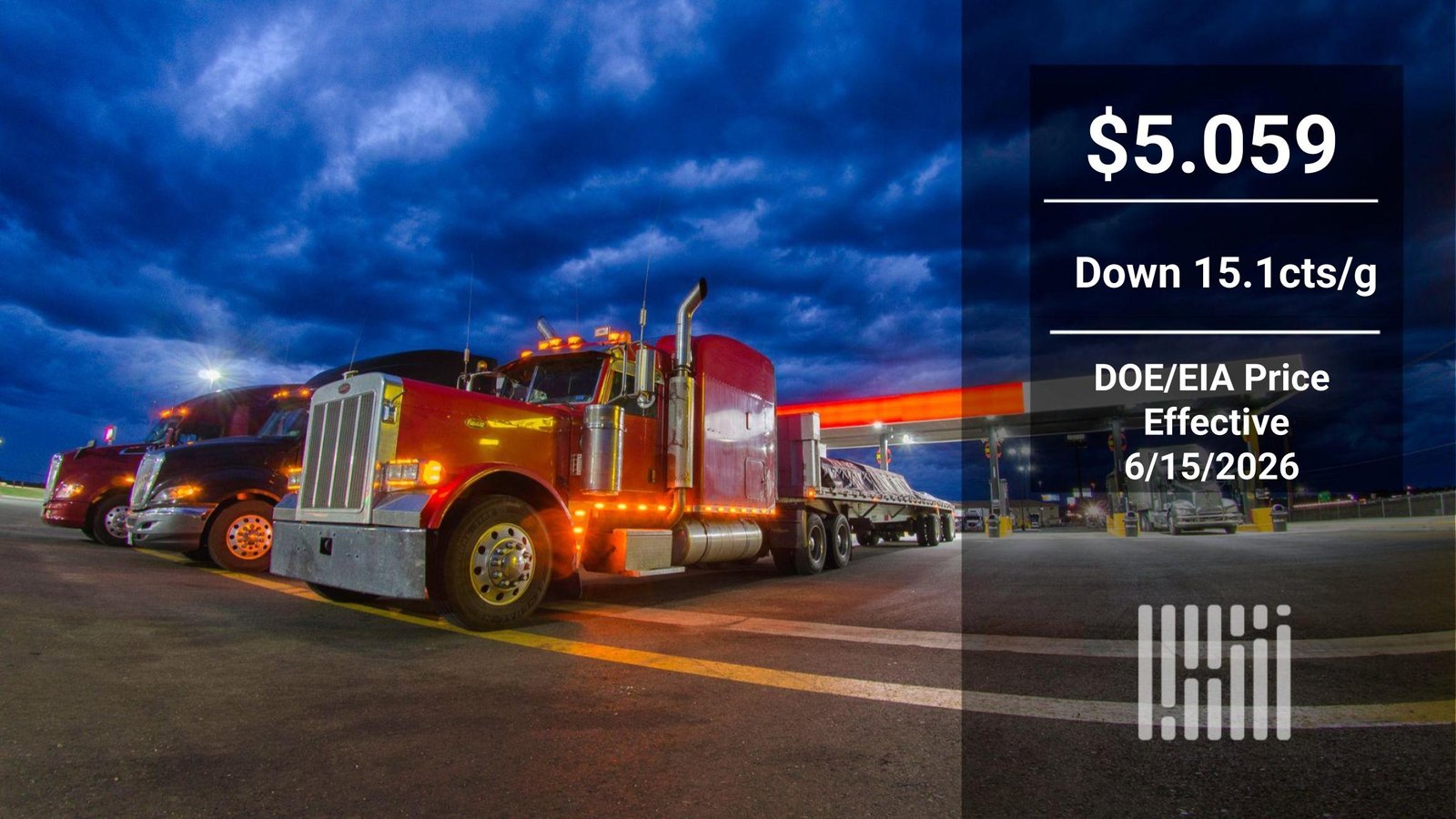

The report comes amid a sharp decline in oil and fuel prices. In the United States, the Department of Energy/Energy Information Administration weekly average diesel price fell by 15.1 cents per gallon to $5.059/g, its lowest level since mid-March, shortly after the initial escalation of the conflict. For comparison, prices stood at $3.897/g before the war began in early March.

Market indicators for ultra-low sulphur diesel (ULSD) also reflected significant volatility. CME settlement prices dropped to $3.1702/g, down 44.24 cents/g in just four trading days, and nearly $1.51/g below the March 20 peak of $4.6084/g. Before the conflict, ULSD had settled at $2.596/g.

While the IEA does not provide price forecasts, its analysis underscores the uncertainty around whether recent price declines will continue or reverse as market “buffers” begin to erode following the ceasefire and evolving post-war supply adjustments.

Supply deficits persist despite demand contraction

On the supply side, the IEA estimates global oil supply will average 102.4 million barrels per day in 2026, down 3.9 million b/d compared with 2025. However, the agency notes that this average masks significant short-term disruptions, including a May production level of 94.5 million b/d, which was 13.6 million b/d below pre-war levels in early March.

Demand has also declined, though not at the same pace as supply. Second-quarter demand is estimated to be down around 5 million b/d year-on-year, or 4.8%, driven by higher fuel prices and product availability disruptions. For the full year, demand is expected to fall by an average of 1.1 million b/d, a sharper revision than previous forecasts, which were lowered by roughly 700,000 b/d.

The IEA noted broad-based consumption declines across multiple regions and sectors, stating that reductions have “spread beyond the sectors and regions that were initially the most heavily impacted.” Asia and the Middle East were identified as the most affected regions, with China, Korea and Japan experiencing particularly steep drops in deliveries.

Buffers, inventories and market stability

A key theme in the report is the role of supply “buffers” that have helped prevent more extreme price spikes despite major disruptions, including the partial shutdown of the Strait of Hormuz and significant production outages.

These buffers include demand destruction, reduced refinery activity in Asia, shifts in global trade flows, strong output growth from the Americas, and large-scale releases from the U.S. Strategic Petroleum Reserve. However, the IEA warns that these mechanisms are being depleted, with global observed oil inventories falling by an average of 3.8 million b/d since March, accelerating to 4.6 million b/d in May.

The agency cautions that continued inventory drawdowns could push stocks to historic lows in the coming months. It also estimates a supply deficit of around 2.1 million b/d between June and August, which would further tighten the market if realised.

Post-war recovery remains gradual

Despite the peace agreement, the IEA expects a slow recovery in global oil flows. Exports are expected to increase gradually but it will probably take months or longer for normal shipping through the Strait of Hormuz to be restored.

The report cited operational constraints such as tanker operators avoiding pre-war routes until mines are cleared, clarity around governance over the waterway and resolution of disputes over transit fees.

At the same time, the IEA’s longer-term outlook shifts sharply in the opposite direction. For 2027, it forecasts global oil supply rising to around 110 million b/d, approximately 8 million b/d higher than current levels, and significantly above pre-war trend expectations.

A market caught between short-term deficit and long-term surplus

Overall, the agency’s analysis points to a structurally contradictory outlook: near-term supply deficits and inventory depletion versus longer-term oversupply risks.

While recent price declines in diesel and refined products suggest easing pressure, the IEA warns that underlying imbalances in production, inventories and trade flows mean volatility is likely to persist as the post-conflict energy landscape adjusts.

- Latest

- Trending

ADVERTISEMENT