A new SAS Aviation Insights report puts some much-needed numbers behind a debate that has so far been mostly theoretical in the aviation industry: what Europe’s e-SAF mandate will actually require, and what it will cost when it becomes reality.

The study, written by SAS Chief Analyst Thomas Thessen, focuses on Scandinavia under the RefuelEU Aviation framework and breaks down how quickly demand for electrofuels could ramp up, and how far the current industrial base still is from meeting it.

At the centre of the discussion is e-SAF itself — electrofuel, or Power-to Liquid fuel. Unlike today’s most common SAF type, which is produced from waste oils and fats, e-SAF is made using renewable electricity, water and captured CO₂. Hydrogen is first produced through electrolysis, then combined with CO₂ into syngas before being refined into jet fuel through either Fischer-Tropsch or Methanol-to-Jet pathways. It’s seen as one of the few truly scalable long-term options, but also one of the most energy- and capital-intensive.

Under RefuelEU Aviation, e-SAF is treated separately from other SAF categories as a Renewable Fuel of Non-Biological Origin, with its own dedicated sub-mandate and penalties if airlines and suppliers fall short. That detail matters, because it turns e-SAF from a climate target into a binding compliance cost.

For Scandinavia, SAS estimates demand starting at around 36,000 tonnes in 2030, rising to more than 60,000 tonnes by 2032. By 2035, the requirement reaches roughly 160,000 tonnes, before climbing to about 330,000 tonnes by 2040. These figures are based on projected regional jet fuel demand of 3.0 million tonnes in 2030 and 3.3 million tonnes in 2040 across Denmark, Norway and Sweden.

What stands out is how quickly this translates into real-world infrastructure needs. With expected production units averaging 60,000 to 70,000 tonnes a year, Scandinavia alone would need at least one dedicated plant by 2032, two to three by 2035, and around five by 2040. At EU level, the requirement in 2030 implies roughly eight large facilities, rising to more than 35 by 2035.

The cost picture is just as striking. Depending on whether supply lags demand or keeps pace, total Scandinavian e-SAF costs could range from €225 million to €850 million in 2030, then jump to €950 million–€3.8 billion in 2035, and reach €1.85 billion–€7.8 billion by 2040.

For passengers, that translates into very different ticket impacts depending on the country. In Denmark, the additional cost per passenger is estimated at 27–105 DKK in 2030, rising to 104–421 DKK in 2035 and 189–803 DKK by 2040. Norway sees similar levels in NOK terms, while Sweden ranges from 34–130 SEK initially up to 233–989 SEK by 2040.

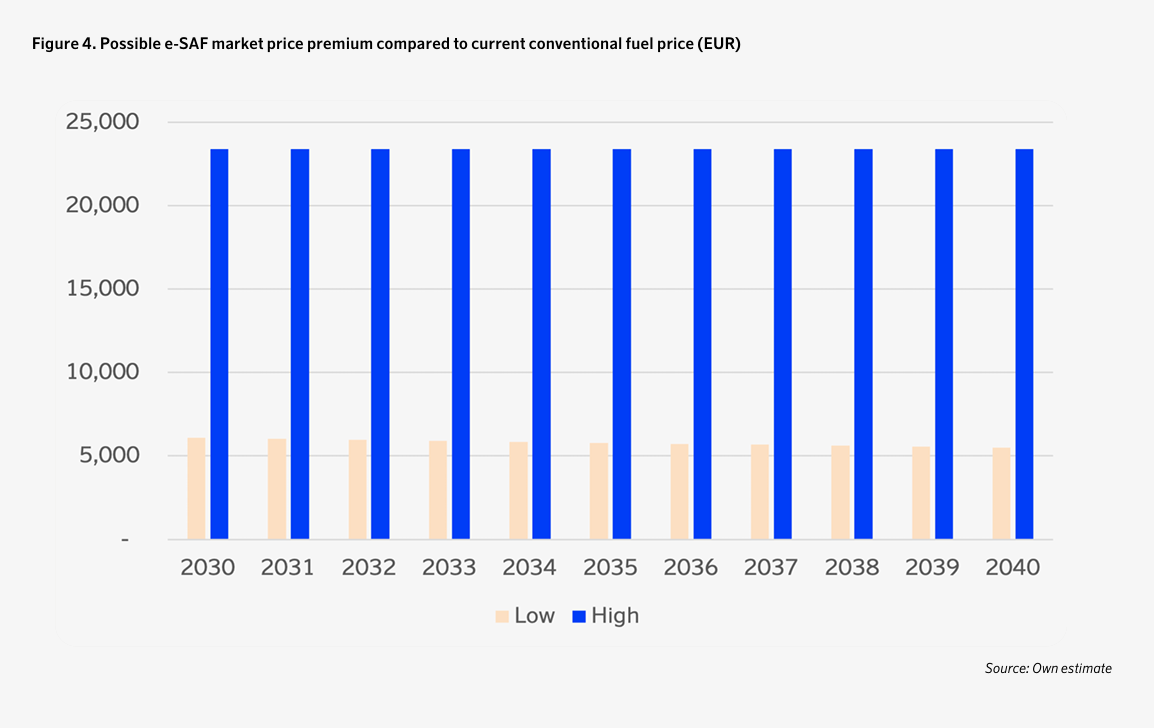

The report also highlights how pricing could behave in practice. If the market remains short of supply, e-SAF prices are expected to track close to penalty levels, which under EU rules must be at least twice the price gap between conventional fuel and e-SAF. Germany has already suggested a penalty level of €17,000 per tonne, while EASA’s estimate sits at €13,922.

In reality, SAS suggests, sustained shortages could push effective compliance costs to around three times the fuel price premium once penalties and make-up obligations are included. That would naturally anchor market pricing even before large-scale production exists.

Beyond the numbers, the underlying message is fairly clear: e-SAF is moving from policy ambition to industrial constraint. The question is no longer whether it will be required,but whether the supply chain can scale fast enough to avoid making it a structural cost burden on airlines and passengers alike.